Liquidity Provider Strategies for Uniswap v3: Loss Versus Rebalancing (LVR)

This installment in the series discusses the concept of loss versus rebalancing (LVR), assumptions behind it and some ways how to mitigate it. LVR is an alternative way how to think about LP profit and loss, different from the divergence loss metric, but complementary to it. It represents the upper bound of the value arbitragers can extract from the system, at the expense of the LPs.

Introducing LVR

The concept of LVR (pronounced “lever”) comes from an academic research group at Columbia University.

- Paper: https://arxiv.org/abs/2208.06046

- Presentation: https://www.youtube.com/watch?v=q5vyJJb-Uyw

The authors start from the observation that divergence loss (DL), i.e. trying to beat HODL, isn’t necessarily the best benchmark for LP profit and loss. In fact, DL mixes different two things:

- Market risk. The LP adds assets in a fixed proportion when creating a liquidity position, but this proportion changes over time, as the relative price of the assets change. As a result, the LP is very likely to have a different exposure to the assets than then hodler, even though they both started with the same asset proportion. The only situation when the LP has the same proportion of assets is when the price reverts back to the starting price; in every other situation the LP has a different market risk. The LP can underperform or overperform the hodler simply because of this different exposure to market prices.

- The risk that comes from the specific trading function of the pooled assets, related to the negative gamma of the AMMs, and the passivity of the LP positions. In short, existing AMMs force the LPs to sell their assets at a stale price, which can be exploited by arbitragers.

These risks can be mostly hedged away — certainly the market risk can, as shown in the last article. However, hedging is not free. In fact hedging costs are directly proportional to the negative gamma value of the position:

- it’s relatively cheap to hedge full-range positions;

- it’s more expensive to hedge wide-range concentrated liquidity (CL) positions;

- it’s most expensive to hedge narrow-range CL positions.

LVR aims to isolate the second type of risks — the AMM-specific and position-specific risks — in a single metric that isn’t affected by the market risk. LVR is proportional to the gamma of the LP position.

Moreover, the divergence loss doesn’t depend on the path price took to get from the initial to the final point. Intuitively, these two are very different situations:

- The price oscillates wildly, but reverts back to the starting point.

- The price remains stable.

Divergence loss is zero in both situations. However, if the price oscillates, both the risk and the opportunity costs are higher. Clearly, volatile pair LPs should be compensated with higher fees in order to fairly price that extra risk. The LVR metric aims to capture this intuition.

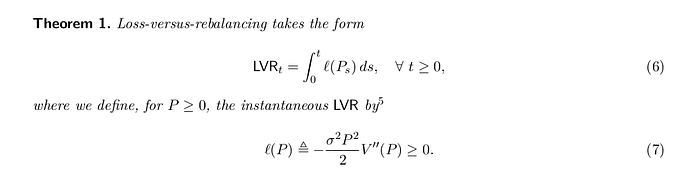

The LVR paper starts from a simple equation:

The authors look at a potential benchmark portfolio that matches the LP’s asset composition, but is traded on a CEX. The idea is that whenever price changes, the CEX portfolio sells one of the assets and buy the other in order to remain in sync with the composition of the LP assets. The rebalancing portfolio is of course also exposed to negative gamma, and is expected to lose compared with a non-rebalancing HODL portfolio. This makes the rebalancing portfolio a more fair comparison target for an LP position than the HODL portfolio.

The profits of this rebalancing portfolio are described by the “Rebalancing P&L” in the equation above. If there are no swap fees, then the LP is going to have a loss compared to such a benchmark position because LPs “trade” at stale prices, and their assets get swapped by arbitragers. This loss accumulates over time and is called LVR.

In the real-world DEX, LPs do recapture some of that loss via swap fees paid by the arbitragers (see the simulations below). In fact, in the 0.3% and 1.0% pools, majority of the loss can be recaptured, provided that the liquidity in the pool is is deep enough. From a practical perspective, it would may be better to call it a “cost”, rather than a “loss”, and remember that the LVR metric describes the theoretical upper bound of the loss.

Example scenario

Bob provides ETH/USDC liquidity on Uniswap v3 1% fee pool, in the price range $1000 to $1100 per ETH. The initial price is $1000 and Bob puts 1 ETH in the pool.

When the price in a CEX changes to $1100, the price in Uniswap becomes attractive for arbitraging. A sophisticated market maker buys ETH on Uniswap and sells ETH on the CEX until the price of ETH on Uniswap becomes $1100. Bob has sold his ETH for the average price of sqrt(1100·1000) = ~1049 USDC, which is now his capital in the pool (there’s no ETH remaining), in addition to the 10.49 USDC he took as a fee.

Alice also initially has 1 ETH worth 1000 USDC, but keeps it in her wallet. When ETH price reaches $1100, she sells it on a CEX, which for some reason has no fees, and provides a willing buyer at that exact price. She ends up with 1100 USDC.

The LVR is 1100–1049=51 USDC. Since it’s greater than the fee that Bob collected, he isn’t profitable according to this model.

Now the price reverts back to $1000. Bob has $20.98 more than he started with, and zero divergence loss: 2.1% profit. At the same time, Alice now buys 1.1 ETH, which translates to 10% profit, more than Bob’s.

LVR in more depth

The authors also introduce the concept of instantaneous LRV. This is understood as the LVR per infinitesimal unit of time. It’s directly proportional to:

- Price volatility squared (σ²).

- The gamma of the LP’s position, which is dependent on the AMM’s trading function, and the concentration factor of the position.

Obviously, in the real world the LPs also collect trading fees, while the rebalancing portfolio does not. In this model, LPs are considered profitable if their fees are larger than LVR, and unprofitable otherwise.

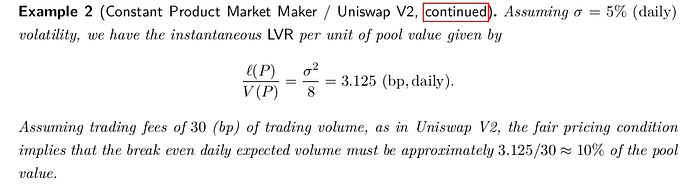

The authors use the second derivative of the pool’s value function, written as V’’(P) in the equation. This is the gamma of the LP’s position, analyzed in the previous article. Mathematically, the gamma of a full-range Uniswap v2-style position is inversely proportional to negative √R³, where R is the price return of volatile asset: i.e. the change in price relative to the initial price at which the position was created.

To sum up, LVR grows with the volatility and gamma: e.g. 2x increase in volatility is going to result in 4x higher LVR.

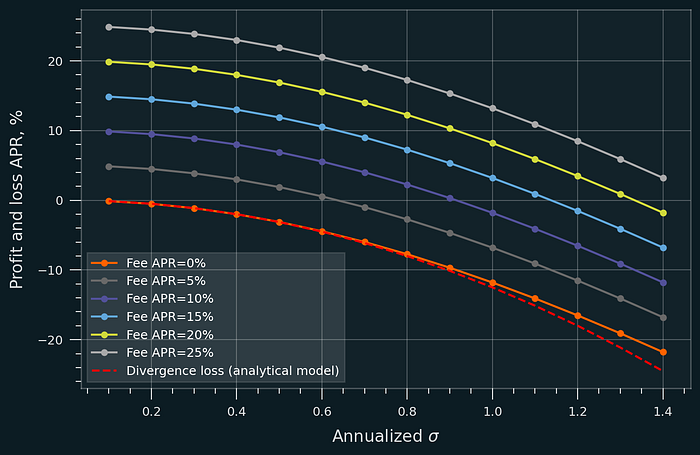

The figure above shows LVR estimation for Uniswap v2-style full range positions. Remember: an LP is considered profitable if fee_return > LVR.

The figure below shows LP profitability depending on σ and on fee APR. The simulations results with fee APR=0% and swap fee f show losses of approximately σ²/8, as expected by the analytical model (shown as dashed line in the figure). For a reference, the yearly σ of ETH since 2020 is ~0.95 -> the required fee APR to offset the loss is ~11.4% for a full-range position.

LVR and DL — are they that different?

If you have read a lot of AMM-related research, that σ²/8 value might be familiar. Indeed, it’s also the minimum amount of fees that need to be collected for a position to be profitable under the divergence loss model. For the expected value of divergence loss in Uniswap see here (v2 and v3) and here (v3).

Alexander Nezlobin’s Medium has an interesting analysis on the connection between LVR and divergence loss (also here on Twitter). His analysis and simulations confirm that the expected value of LVR is the same as the expected value of divergence loss. However, he shows that LVR has smaller variance than divergence loss.

This equality between LVR and EV(DL) is an interesting result, although the actually realized forms of LVR and DL are very different. The latter does not depend on price path at all, and has a market risk component that LVR does not include.

While in some situations LVR can be replaced with EV(DL), it isn’t always the case. For example, let’s assume a pair with stable coins that always revert to their initial price, but have random oscillations in relative value. The expected value of divergence loss is close to zero, while LVR, as intuitively understood, is going to grow with time.

A caveat that I need to stress: we need to consider the expected value of divergence loss rather than the divergence loss itself. The former depends on the volatility, the latter on just the initial and final prices.

Assumptions behind LVR

1. There is a CEX or some other alternative venue with deeper liquidity where price discovery occurs. This is not true for many long-tail assets, which are primarily or exclusively traded on Uniswap. The rebalancing portfolio does not exist for such assets. While the LVR value can still be computed for these assets, it lacks practical significance.

2. There are LPs, “uninformed traders”, and arbitragers. The arbitragers trade without paying trading fees. This a technical simplification that has some impact on the results; a follow-up paper from the authors shows what happens in the more realistic model when arbitragers are also required to pay fees.

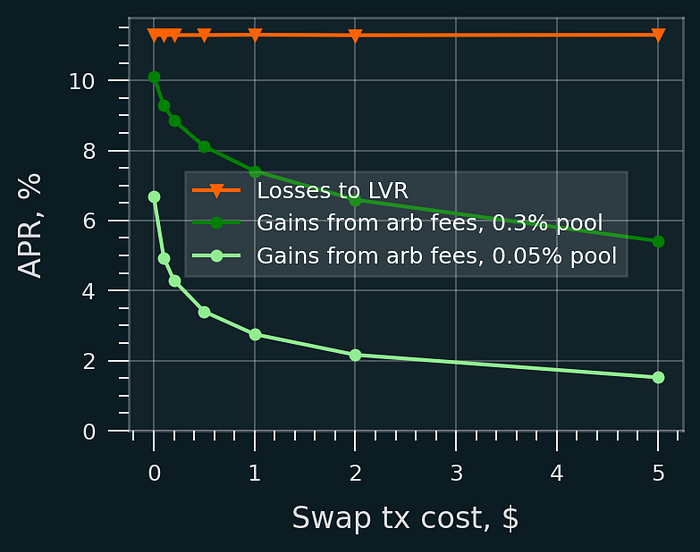

For a start, I did quick price simulations with 0.3% swap fees, and realistic block times & transaction costs. The results show that a significant part of the LVR is captured as liquidity provider fees.

- If transactions are free (zero fixed swap cost), then large part of the LVR is immediately compensated with LP fees from the arbitrage transactions. The exact amount depends on the swap fee, but it can be 80–90% as show in the graph (for 0.3% swap fee pool).

- If transactions have non-zero execution fees, then then recaptured LVR proportion goes down, because arbitrage trading frequency is reduced a lot.

- The recaptured LVR also depends on the the swap fee in the pool.

See the figure below, but take the x axis in the figure below with a grain of salt: the exact impact of the Tx fee depends on the liquidity depth in the pool: 10x deeper liquidity is going to have the same effect as 10x cheaper transaction fees.

3. Arbitragers and LPs engage in a zero-sum game. This is true only if we don’t add any other actors to the game, but might change if consider the market as a whole. For instance, arbitragers have to pay transaction fees, which benefit third parties like ETH stakers & holders. However, a more interesting question is whether LPs always are worse-off then holders because of the arbitrage?

One trivial case is a stable pair, which only has random oscillations in the price. LPs are going to beat holders here: LPs earn fees from arbitragers every time the mutual price has large enough oscillations (i.e. diverges more than the pool’s fee rate + tx costs).

But can LPs beat HODL even for volatile asset pools, assuming the worst case scenario when only arbitragers are trading that pair? (I.e. all swap volume is “toxic flow”.) The answer is dependent on market conditions, but the expected value analysis is probably negative. A blog post from 2020 in the Paradigm’s website claimed that LPing even in these conditions can be much better than holding. Specifically, the showed this under two specific assumptions: first, that the volatile asset price goes up with time; second, that the volatility is within a specific range (high, but not too high). However, some have pointed out that there might be some problems with their math model. Unfortunately, the original blog post now seems to be removed, as Paradigm has restructured their webpage. I cannot comment on the accuracy of these results, but here’s my Twitter thread discussing them.

4. Asset prices follow Geometric Brownian Motion. Conceptually the LVR still applies under different price models, however, the exact values of LVR presented in the paper might not be correct if the model’s assumptions are violated. However, the authors have later extended their work to also show that the same result holds even if volatility is not a constant, but instead is a time-dependent process, which is a more realistic assumption.

5. The LPs have hedged their exposure to price risk. This is obviously a big assumption that’s not true for many LPs.

Mitigating LVR

LVR is essentially caused by LPs “trading” at stale prices. It can be mitigated by either making the prices less stale, or by increasing the fee income of the LPs. Some ideas follow.

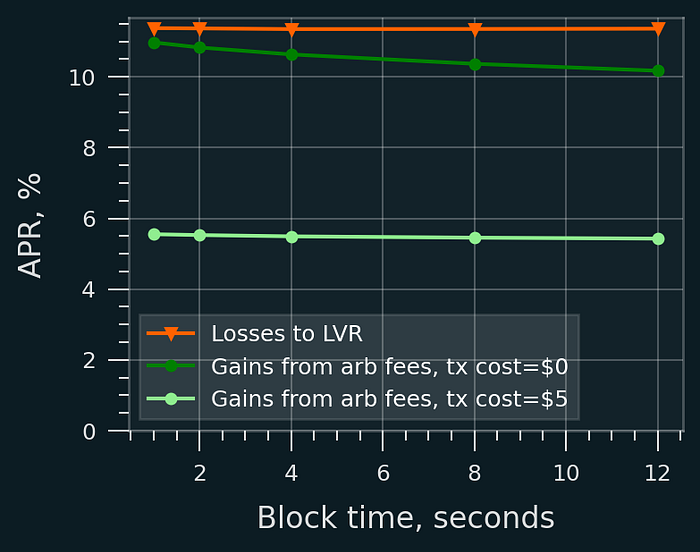

1. Increase arbitrage trade frequency by decreasing block times. While shorter block times are not expected to reduce LVR, they might increase the swap fees collected by LPs due to higher swap volume. However, my simulations failed to confirm any significant benefits for the LPs in realistic conditions! See the figure below. While there are existing simulations that show significant benefits, they use the assumption that transaction fees (gas costs) are zero.

Swap fees only seem to be depend on block times when transaction fee is zero (see the figure above), allowing arbitragers to trade even when the smallest of profits can be captured. Nevertheless, short block times might eventually be better for LPs due to other reasons. An empirical comparison between L2 (Arbitrum, Optimism) and the mainnet would be interesting.

2. Use a CEX-sourced oracle to tell the pool “true” price of asset. This requires protocol-level changes in the AMM itself, and I really don’t like this approach: it’s not robust, permissionless, and does not scale to the long-tail assets. The future of DeFi is in oracle-free protocols.

3. Dynamic fees. While Uniswap v1-v3 do not have dynamic fees, the LPs can and probably should monitor volatility and relocate their liquidity to higher fee tiers when needed. In v4 much more advanced dynamic fee options will be enabled thanks to hooks.

4. Execution speed-dependent fees. The idea is to penalize trades that must be executed rapidly (arbitrage trades) while lowering fees for trades that can wait for multiple blocks (uninformed trades). This likely requires AMM-level changes.

5. Change the payoff distribution between the participants. For instance, if there were some ways how to capture the transaction fees paid by the arbitragers and pay them directly to the LPs, then LPs could be incentivized to provide more liquidity. A LVR reduction through MEV recapture is technically possible to integrate in Uniswap v4, via hooks.

Additionally, an L2 or L3 chain created specifically for DeFi trading applications might support this out-of-the box. Uniswap chain, anyone?

Some additional ideas from Paradigm’s Dan Robinson are listed here here, including distinguishing arbitrage and non-arbitrage flow, and more specific MEV-related ideas.

Key takeaways

- LVR represents the maximal arbitrage extractable value at the cost of LPs providing liquidity in AMMs. It appears due to LPs trading at stale prices. Some of the LVR is extracted as CEX-and-DEX arbitrager profits, some goes to block builders, and some is recaptured by the LPs via fees.

- LVR is relevant to volatile short tail (ETH/USDC, WBTC/USDC, etc) pairs, although some of the ideas do carry over to stable pairs and long-tail assets. Normally LVR assumes that arbitragers trade between AMM liquidity pools and price discovery zones, such as a CEX with deeper liquidity.

- The divergence loss metric also includes market risk, while LVR does not include that; instead it focuses on the AMM-specific risks, which cannot be hedged as easily as market-risk exposure can.

- LVR can be mitigated in several ways, but most of them are only available to protocol and blockchain designers, not LPs themselves.

- LVR is an important concept that is required to better understand LP at a deep level. Nevertheless, it doesn’t obsolete divergence loss as a key metric for LPs. The beauty of the divergence loss is that it uses the HODL benchmark, which is a realistic alternative option for any LP. Of course, there’s no reason for all LPs to converge to a single standard at all: one-size-fits-all approach is not realistic, as LPs have different goals.

Acknowledgements. This work received financial support from the Uniswap Foundation. Thanks to Jason Milionis for explanations & comments on a draft version.

Disclaimer. This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. This article was written in the author’s free time and is not related to his professional activity or his employer. This post reflects the current opinions of the author, which are subject to change without being updated.